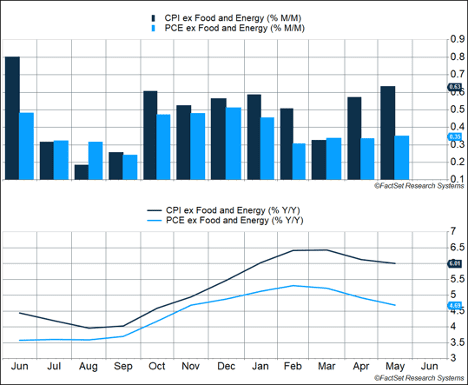

The Personal Consumption Expenditure (PCE) Price Index increased 0.6% in May, after rising only 0.2% in April. PCE inflation is an alternative inflation measure to the Consumer Price Index (CPI), which is released earlier. The two measures both show inflation to be very high, but the CPI indicates prices have risen 8.6% in the last year, while PCE inflation has increased only 6.3%. The biggest difference is the basket of goods that make up each measure. For example, PCE inflation includes a wider range of medical costs, which have not increased as much as energy prices. Energy comprises 7% of the CPI and just 4% of the PCE. The Fed has indicated it favors the PCE measure, modified to exclude food and energy. PCE ex food and energy increased just 0.3% as gasoline prices rose significantly in May.

Key Points for the Week

- Core PCE inflation, which excludes food and energy, rose 0.3%.

- Personal consumption rose 0.2% as higher spending on services overcame a decline in spending on goods.

- The S&P 500 fell 20% in the first half of the year — its worst first-half performance since 1970.

One trend likely to help the Fed reduce inflation is increased spending on services. Services spending rose 0.7% while goods spending dropped 0.7% last month. Services account for a larger share of the economy, so the net effect was a 0.2% increase in overall spending. Service inflation has been lower than goods inflation, and decreasing goods spending is likely to reduce price pressures on some items in short supply.

The S&P 500 declined 2.2% last week as markets became more concerned about the risks of recession in the coming year. The index of large-cap U.S. stocks fell 20% in the first half of the year. Global stocks matched the S&P 500’s decline. The MSCI ACWI sagged 2.2%. Because the concern was more about recession than inflation, bond prices increased. The Bloomberg Aggregate Bond Index added 0.4% last week and posted its second week of gains. The Department of Labor’s update on the U.S. employment situation leads the list of economic releases this week.

Figure 1

Figure 2

Five Reasons to Expect a Better Second Half

This year’s Fourth of July celebrations weren’t for the first-half market performance. The S&P 500, including dividends, declined 20% in the first six months of the year. The fall represented the worst first-half market performance since 1970. Emotionally, this market has taken its toll through a decline that started the second day of the year and accelerated in the second quarter. High inflation has been the biggest challenge, and every time we get gas, buy groceries, or check the market we are reminded of it.

The propensity in down markets is to expect current trends to continue. In difficult markets, it is also easier to focus on known negative factors that have proven to be challenging. Yet, as we enter the second half of the year, there are strong reasons to expect improvement. Here are five forces we believe will make the second half of the year more attractive than the first.

- Much of the bad news is already reflected in market prices.

The first half of 2022 contained a lot of bad news for markets, and prices fell in response. Inflation continued to increase, COVID shutdowns slowed the repair of supply lines, and Russia invaded Ukraine. In response to high inflation, the Federal Reserve pivoted and raised interest rates three times, once by 0.5% and once 0.75%. Europe reacted to Russia’s invasion of Ukraine by drastically reducing its purchases of Russian oil, contributing to slower economic growth and higher inflation. While those events had negative consequences, remember the market has already reacted to the news. With the S&P 500 20% lower than at the start of the year, it’s hard to argue that markets have ignored what has occurred.

- Inflation seems to be moderating.

The Fed’s favorite measure of inflation increased 0.3% for the fourth consecutive month. But the Personal Consumption Expenditures Price Deflator (PCE) ex Food and Energy has moderated in recent months. From October to January, core PCE increased approximately 0.5% per month. An increase of 0.3% is still too high. Multiplying it by 12 creates a simplified annual inflation rate of around 3.6%, which is well above the Fed’s target of 2%. But our view is the steps the Fed is taking are starting to work, and additional hikes will contribute to slower price increases in coming months.

- Political uncertainty is ebbing lower.

In the presidential election cycle, the second year of the administration is statistically the most challenging. Domestic political uncertainty has made this year even more so. House and Senate majorities are very narrow, and both houses of Congress could switch parties in November. The Supreme Court has been full of surprises, and the Jan. 6 commission has added to the mix. By the fourth quarter, and possibly even the third, polling data will provide some clarification on how midterm elections will turn out. The high inflation has also undercut any desire for a major spending initiative. Because the last support package seemed to feed inflation, avoiding high government spending should help reduce inflationary pressure.

- Much of the economy remains strong.

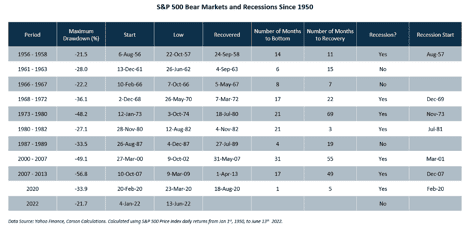

While the current bear market is the 11th since 1950, it is only the fourth to occur outside of a recession. Non-recessionary bear markets are usually shallower, averaging a 28% decline, compared to an average 39% decline for recessionary bear markets (Figure 2). This week, the government will release the Job Opening and Labor Turnover Survey (JOLTS) for May and the Employment Situation report for June. The ideal result is decent job creation while companies choose to pull back open positions to reduce the excess demand for labor.

- The system works.

Hopefully, as investors lit off fireworks celebrating our country’s founding 246 years ago, they appreciated the resiliency of the American system. Investors who focus only on the short-term swings in inflation, political winds, and Fed policy should take note of the longer-term success of this republic and how people and equity markets have prospered. Even with two bear markets, inflation and a global pandemic, the S&P 500 is up double digits over the last 10 years.

The key is to find the right balance. This has been a tough year, and we will continue to monitor a wide range of near-term risks and how they affect markets. Because many of those risks are already reflected, at least partially, in current prices, the more impactful data points may be those showing how a system with a long record of success is recovering.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

Bureau of Economic Analysis. 6/30/22.https://www.bea.gov/news/2022/personal-income-and-outlays-may-2022

Bureau of Labor Statistics 06/10/22 https://www.bls.gov/news.release/cpi.t01.htm

Federal Reserve https://www.federalreserve.gov/monetarypolicy/openmarket.htm

Compliance Case # 01420404